There is so much going on in the Australian telco market that it is hard to keep up. Each of the main telcos: Optus, Telstra, Vodafone and Sydney based TPG are finding ways to outdo each other, while the Mobile Virtual Network Operators (MVNO) are trying to get a look in the door too. Many of these service providers have had to adapt due to criticism in relation to service quality and uncontrolled outages. One wonders what the whole network would be like without this competitive element. Telstra for one has increased its revenue through its mobile services which in the years between 2015 and 2016 was $10.4 billion making up 40 percent of its revenue compared to a decade ago when this revenue earner only accounted for 22 percent at less than $5 billion.

Contracts being ditched by mobile customers

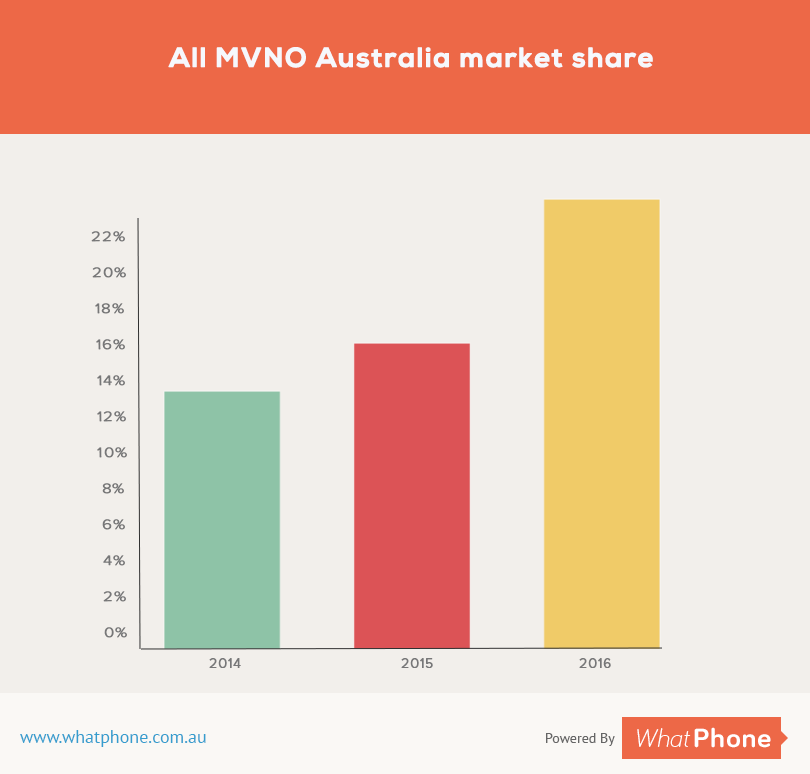

The competition between the big telcos is hotting up as Australia’s mobile customers are losing interest in taking on purchasing phones tied to contracts. Recent research has revealed that more than 50 percent of mobile customers are not locked into a contractual agreement. This means the larger telecommunications players can’t depend on loyalty any longer as customers are far more intent on shopping around for the best deal.

The research firm Telsyte came out with an estimate that of the 25 million handhelds in use in the middle of the year more than half were not on contracts. The recent trend over the last 12 months has indicated that 66 percent of mobile customers who changed their mobile provider chose plans with no contracts. Coupled with these trends is the development of competitive mobile prices offered by MVNOs like Woolworths and Kogan, which are becoming attractive alternatives to the big 3 while offering at least the same 4G coverage which is what consumers are after.

Broadband Being Developed as a Competitive Advantage

How the telcos are faring

- TPG:

Broadband is being used as a way of growing customer base. As TPG has grown, it is biting into the market share for broadband following its purchasing late in 2015 of iiNet. - Optus:

Optus is following closely with plans in the not too distant future of providing broadband services to 8 million premises which is double what it offers at present. Optus was up to a point reporting a decline in revenue but this was reversed in 2015 when it experienced a 6.7 percent rise. - Vodafone:

Vodafone (VHA) has in recent years been experiencing a steep decline in revenue due to the customer base withdrawing from its services due to dissatisfaction, but last year this was reversed with a rise of 2.9 percent in revenue in the 1st half of the year, with a 2.1% rise in its MVNO subscriber and retail base. - Telstra:

Telstra still has the largest overall share of the Australian telco market. It receives 62 percent of the country’s revenue in that area. It hasn’t been faring quite so well in relation to broadband which has seen a fall in revenue. Telstra gained some advantage in being the first of the telcos to deploy LTE but Vodafone and Optus have caught up in this respect. It also allegedly grew its revenue at one point due to Vodafone customers tired of the poor service looking for an alternative.

Cool speeds for Future Mobile Connections

There is a reasonably large market in Australia with 31.4 million mobile subscribers recorded at the end of 2015. This is a lot considering the total population is just a little over 21 million. Subscriptions to mobile broadband are over six million. Around 25 percent of these are using LTE networks with this set to rise in the short-term. There is still more work to be done on LTE, but 5G interest is taking over which will be designed in such a way that billions of devices will be able to connect through it.

Telstra has already announced its closure of 2G infrastructure because it only takes 1 percent of its traffic at present. The rest of the MVNOs will be following this trend in the not too distant future and by 2025 4G will be non-existent, with 5G and LTE becoming the norm. This will see increases of speed from the current 100Mps to breakneck speeds of 20GBps. This will be up and running in the U.S. by at least 2020 with some rollout taking place as early as next year by Verizon. 20GBps will mean speeds that overtake those currently found on most home broadband today.

Up to now the fastest speeds that have ever been seen are on Google Fiber in the US, which reaches speeds of up to 1Gbps. This makes the projected speeds for 5G standing at 20 times faster than that.

Key developments to attract customers

- iiNet sets up to 30,000 Wi-Fi hotpots in the nation’s capitals and offers limitless data plans

- Telstra releases Air Wi-Fi network;

- Optus plans to re-enter DSL market using the NBN;

- Draft standards released in relation to NBN and vectored VDSL2 provisions.

NBN is slowly moving forward

Coupled with other developments the broadband sector via NBN is expanding through the use of fibre access which is opening up the opportunity for an increase in the growth of the cable and DSL sector which is also improving its technology. The digital subscriber line (DSL) sector is holding its own as operators are tending to make more use of VDSL and undertake further trials of G.fast technology which is a DSL protocol for local loops of less than 500 m.

Its usual performance targets range from 150 MBps to1 GBps, depending on the loop’s length with short loops achieving greater speeds. It can deliver much greater data capacity using older copper infrastructure. Much of the hybrid fibre-coaxial (HFC) used in the broadband network operated by Optus and Telstra has been the subject of underinvestment, is to be incorporated into the NBN, and along with commercial DOCSIS3.1 technology being deployed in 2017. Cable investment is on the cards again.

Rural customers to benefit soon from superfast broadband

NBN roll out has recently been occurring at a faster rate with the most recent proposals being for FttP, FttB and services which are copper-based, running a Superfast Broadband Access Service (SBAS) which is out to benefit rural customers. Even though this technology is not seen as the best, added to it are Telstra’s and NBN Co aim to incorporate G.Fast. So far, speeds of 600MBps have been achieved in Melbourne trials.

Spectrum increases to benefit rural customers

There is currently a spectrum shortage but the ACMA has got into the process of reallocating th spectrum that is available in a number of bands to be used by LTE. The government announced last year the intention of reallocating the frequencies 1725–1785MHz and 1820–1880MHz ranges for regional Australia by issuing new licenses through an auction.

Competition hots up with Vodafone losses continuing while Telstra, Optus, Aldi and Amaysim gain

As has been mentioned earlier there is a growth in the no-contract mobile sector with Telstra, Optus, Aldi Mobile and Amaysim being the key beneficiaries while Virgin, Vodafone (VHA), TPG and some other MVNOS have lost mobile customers.

With interest in taking up contracts for mobile communications waning, the no-contract group now makes up 15.4 percent while last year it stood at 11.9 percent. Post-paid subscribers dropped from 55.6 to 53.4 percent while prepaid fell from 32.6 to 31.2 percent. In the same period Optus showed the largest growth in its market share of mobile subscribers with a 1 percent rise in the 12 month period up to September now taking 22.3 percent. It seems that 40 percent of Optus’ new customers were transfers from Telstra. Its growth areas were with no contract customers and post paid customers. The market share for post paid customers 24.3 percent and no contract 19.5 percent. Its pre paid customers remained at stable numbers.

Telstra still seems to be a winner, having almost 40 percent of the total market share with the biggest rise seen in pre-paid customers in the last 12 months.

How the MVNOs have performed in the last year

- Aldi Mobile followed Optus in its growth pattern with a gain of 0.8 percent therefore taking 3 percent of the overall market share. Its prepaid subscriber numbers rose the most followed by its no contract subscribers. Kantar the telecommunications surveyor stated that Aldi’s new customers were drawn from Optus’ customer base. The main attraction is its cheap call packages.

- Amaysim saw slight gains despite having spent AU$70 million on buying Vaya earlier in the year and it now takes nearly 5 percent of the market share.

- Boost Mobile saw a similar trend and now has its hands on 0.7 percent of the mobile market. Its largest sector being prepaid customers.

- VHA which is a combination of Three, Vodafone and Crazy John’s has lost some of its market share resting currently on 14.9 percent. Its losses were in the prepaid area with slight gains in post-paid.

- Virgin Mobile followed VHA’s trend falling in most areas with its total share now standing at 5.2 percent.

- TPG and iiNet together now make up 2.7 percent of the mobile market with recent falls in all sectors.

Some of the other MVNOs saw a drop in customers too with this group of mobile providers now taking 6.4 percent of the market share.

How well the telcos were ranked for customer loyalty and complaints

Loyalty: Kantar revealed Telstra has 94 percent customer loyalty, while Aldi Mobile attracted 92 percent.

Complaints:

- It seems that Vodafone’s customer losses were related to the number of complaints about them. In the July to September quarter there were 6.2 complaints for every 10,000 services (SIO) which was 66 percent up on the previous quarters 3.8. Vodafone went through in September a 4G outage which affected voice, text messaging and data and allegedly due to a router issue. Vodafone considered that their complaints only matched industry averages and the outage was not responsible.

- Optus saw a rise in complaints in the last quarter, attracting 7.2 for 10,000 SIO, a rise from 6.7 experienced in 2015.

- Telstra’s complaints weren’t quite as high as other telcos but stand at 6 for 10,000 SIO.

What’s in store for the near future?

The latest news on the telecommunications front is related to concern from Telstra’s one million shareholders who are wondering what Telstra’s investments are going to reap for them in the next year or so. John Mullen, Telstra’s chairman, is worried too. He took a swipe at Vodafone, stating that the company is after a cheap ride through its push for customers of other telcos to use Telstra’s regional areas mobile network. Telstra is obviously opposed to the plan after having spent billions creating its own mobile network.

This has allowed it to stand out from the other telcos that are its competitors. But Vodafone (VHA), regional communities and farmers see things somewhat differently. The concern by Mullen was raised after the Australian Competition and Consumer Commission’s staged a domestic roaming inquiry. The ACCC has been asking industry and consumers whether it should allow domestic mobile roaming services. If it succeeds, Telstra will have to let competitors’ customers on to its network in regional and rural areas. He believes this proposal if it goes through could affect shareholder value and shareholders have the right to lodge a complaint about this proposed action.